Table of contents

Kering Group earned € 20,3 billion in the financial year 2022 with a 15% boost compared to FY 2021 and € 10,13 billion in the first half of 2023 with a 2% increase compared to H1 2022. When it comes to the recurring operating income, 2022 has improved by 11% and H1 2023 by -3% due to an investigation occurring through the Houses of the group.

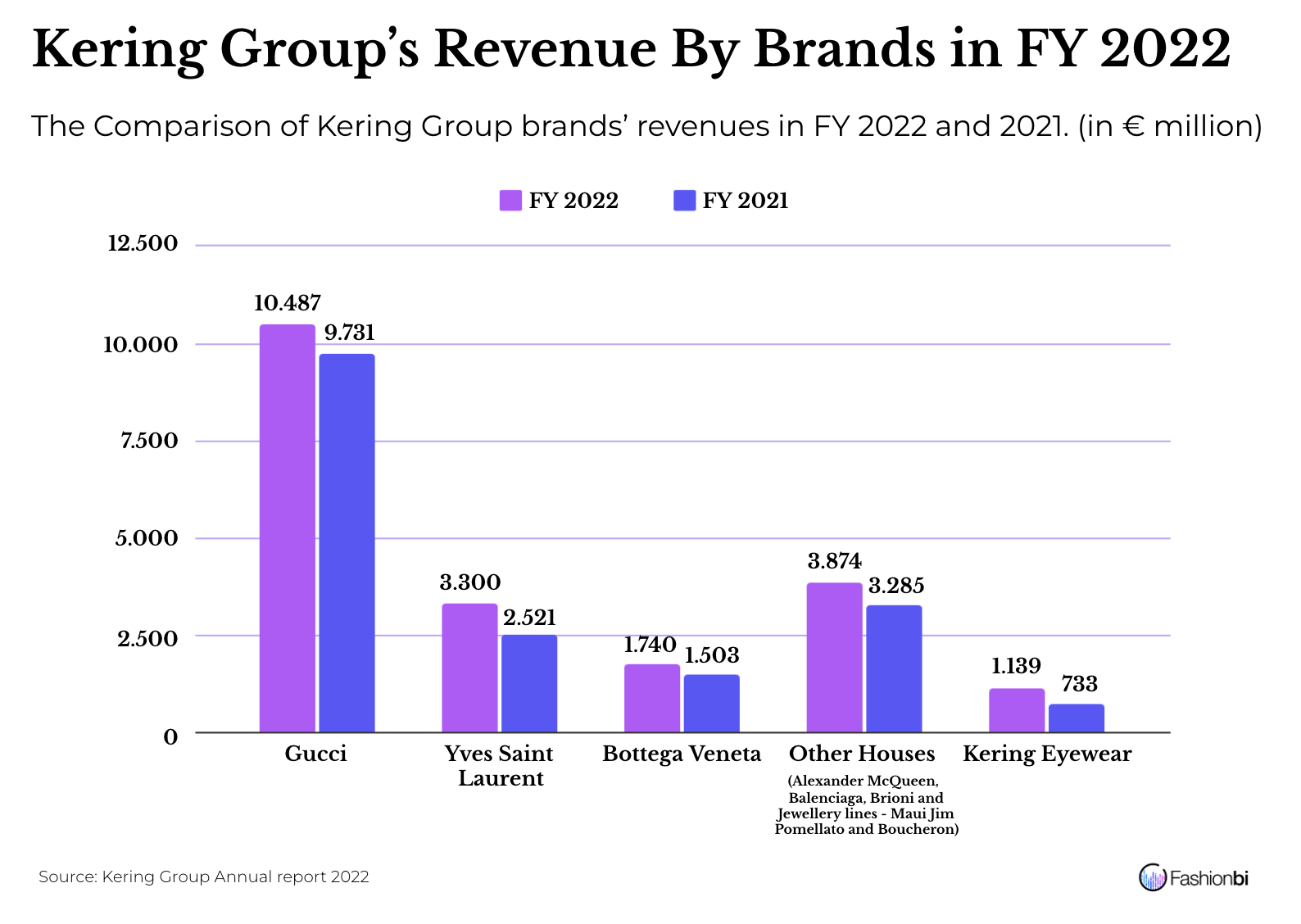

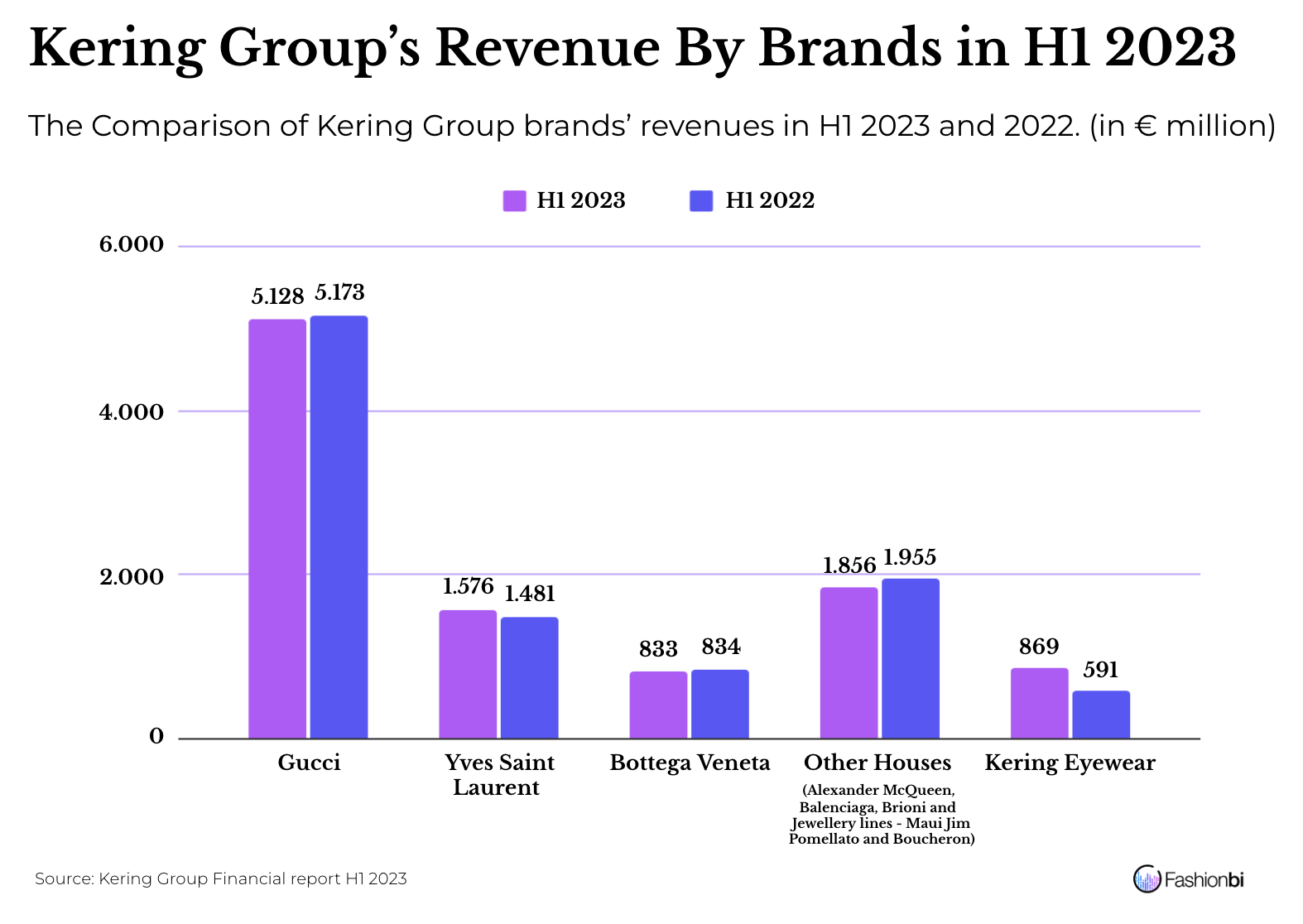

Revenue by Brand

Gucci

In FY 2022, Gucci generated around 64% of the Kering revenue, accounting for €10,5 billion, with an 8% reported change from 2021. Even though the wholesale revenue was in a constant state, directly operated retail revenue was raised by 1%. The brand’s turnover faced a 14% depth on a comparable basis in Q4 2022. The sales of directly operated networks were down by 15% and were deeply influenced by China’s zero-Covid policy during the quarter. Gucci’s recurring operating income was €3,7 billion and its recurring operating margin was around 35,6%, showing the group's investments towards the brand’s growth in the future. During the year, Gucci diluted its margin on the supported investments and established new models and organisational structure on the key sectors including Creative Direction, Communications, Merchandising, and Regions. The brand focused on continuing its growth strategy and reworking on the core business with new launches in Leather Goods. There was a positive Average Unit Retail in all the product categories. By the end of the year 2022, Asia Pacific owned 36% of Gucci’s revenue with North America (29%) and Western Europe (22%) at the forthcoming positions.

In November 2022, Kering announced the departure of Alessandro Michele as the Creative Director of Gucci. In January 2023, the group and the brand made a statement that Sabato de Sarno will be the next Creative Director of Gucci.

In H1 2023, Gucci’s turnover was €5,1 billion, with a decline of 1% on the report. The directly operated stores garnered a 1% rise whereas wholesale dropped by 3% when compared to H1 2022. The revenue of the brand climbed 1% (comparable basis) in Q2 2023. The directly operated retail network increased by 1% due to the high demand for the brand’s exclusive products from travel, leather goods, and women’s lines. Its recurring operating income accounted for €1,8 billion and a recurring operating margin of 35,3%, circling the investments for Gucci’s inventive strategies. The house recorded a favourable performance in travel, womenswear and handbags. It also maintains its investment towards strategic initiatives such as client experience, stores and communications. So far, the Asia-Pacific region holds the highest percentage of total revenue, amounting to 42%, followed by Western Europe and North America (22% each).

Yves Saint Laurent

Yves Saint Laurent produced €3,3 billion in 2022, with a 31% increase compared to 2021. The turnover of directly operated stores rose by 28% and wholesale sales went up by 6%. In Q4 2022, the revenue had a 4% rise on a comparable foundation, driven by the great performance of the DOS network (up by 7%). The wholesale revenue dropped by 13%. The brand reached a recurring operating income of more than €1 billion, which resulted in its recurring operating margin increasing by over 30%. The product categories RTW and leather goods had a notable growth rate. Moreover, the brand had successful Fall/Winter collections and carryovers. In the fourth quarter, Saint Laurent had a 13% revenue dedicated to its exclusivity in distribution and retailization. The label went on to invest in client experience and visibility with more focus on domestic clients and brand growth. When it comes to regions, North America is in first place with 33% of the total revenue, Western Europe (31%) in second and Asia-Pacific (25%) is the third.

In the first half of 2023, Saint Laurent yielded €1.6 billion as revenue with a 6% growth as reported change. The turnover of the DOS network has soared by 11% on a comparable ground and wholesale revenue went down by 10%. The house is on-process to consolidate this channel. Q2 of 2023 gave a revenue that had a 7% increase on a comparable basis due to the sales hike of 8% in the DOS network which was driven by the leather goods and ready-to-wear lines. The recurring operating income amounted to €481 million with a recurring operating margin of 30,5%. It faced a sustainable growth in Leather Goods and RTW categories, with successful results in Spring/Summer 2023 collections and the new Fine Jewellery launch. The brand is reinforcing its production capacity. In this period, Western Europe overtakes North America (27%) with 31% and Asia-Pacific holds 30% of Saint Laurent’s turnover.

Bottega Veneta

With its perennial positioning, Bottega Veneta's revenue totalled €1,7 billion, up by 16%. This rise was by the DOS channel which increased by 15% while the wholesale revenue was stable. In the fourth quarter of 2022, the revenue grew by 6% on a comparable foundation with the help of healthy performance in the DOS network (+4%) and wholesale (+13%). The brand has a strong performance in Western Europe, Southeast Asia, and Japan. There were price increases in several categories, along with strategy on iconisation. Customers showed a high desirability on the new collection. The label focused on providing creative retail experience, store expansion and relocation, brand equity, clienteling and impressive communications.

Bottega Veneta generated €833 million (stable as reported) in H1 2023. Even though the wholesale revenue dropped by 13%, the DOS network turnover increased by 6%. In the second quarter of 2023, the revenue hiked by 3% with the support of favourable growth in the DOS channel (an increase of 7%). The recurring operating income accounted for €169 million with a recurring operating margin of 20,3%. RTW and Leather Goods were named as the best performing lines. Further investments have been funded for the stores and communications to elevate the brand positioning and resonance.

Other Brands

From the other brands, the group generated €3.9 billion in revenue with a rise of 18% in 2022. This elevation was because of the DOS channel with a sales increase of 27%. Whereas, the sales wholesale was down by 6%. Balenciaga performed well in 2022, despite its Gift Shop campaign ad scandal in November. Following that, the brand’s biggest collaboration with Adidas was put on hold. Alexander McQueen had a great year with good sales in the ready-to-wear and handbags line. In March 2022, ##Gianfilippo Testa## was appointed as the CEO of Alexander McQueen. Brioni has recovered from the previous year’s fall. Kering’s jewellery line is performing very well with excellent outcomes. Pomellato is expanding its reach in Japan and Western Europe. Boucheron reported strong growth and Qeelin went on to develop at a quicker pace. They earned €558 million of recurring operating income with a 14,4% recurring operating margin.

The other brands produced €1.9 billion of turnover, which is a 5% drop as reported, in H1 2023. However, they had a notable improvement from the first to the second quarter of 2023. The DOS network’s sales were up by 8% with wholesale falling by 27% due to the pursuit of all the brands to streamline this channel and to display a mixed American market. In Q2 2023, the revenue went up by 9%. Balenciaga has started to retrieve from its fall, driven by sales in the Asia-Pacific region. Alexander McQueen’s performance was raised in the ready-to-wear category and Brioni had a good improvement with its bespoke, leisurewear and formal wear. The jewellery lines - such as Pomellato, Boucheron and Qeelin - have continued their rigid trajectory with a double-digit growth rate. They produced €224 million as recurring operating income with a recurring operating margin of 12,1%.

Kering Eyewear and Corporate

In 2022, Kering Eyewear crossed a billion euro in revenue, with a 58% climb as reported. The turnover amounted to €1,1 billion, validating its successful strategy and the tireless contribution from Maui Jim (which was acquired in March 2022) and Lindberg. In the fourth quarter of 2022, the revenue went up by 30% on a comparable basis due to the brand’s noteworthy performances. Its recurring operating income was €203 million, around 2,5 times higher than that of 2021. After subtracting the costs of corporate, recurring operating income summed up to €88 million.

While considering the first half of 2023, the revenue reached €869 million with a 51% increase driven by Maui Jim’s favourable works. In Q2 of 2023, the sector had growth of 21% in sales with its fortunate improvements in brand portfolio. The recurring operating income hit €186 million. With the corporate cost accounting for €123 million, the income is deducted to €63 million. In March 2023, Kering Eyewear acquired UNT, a French manufacturing company.

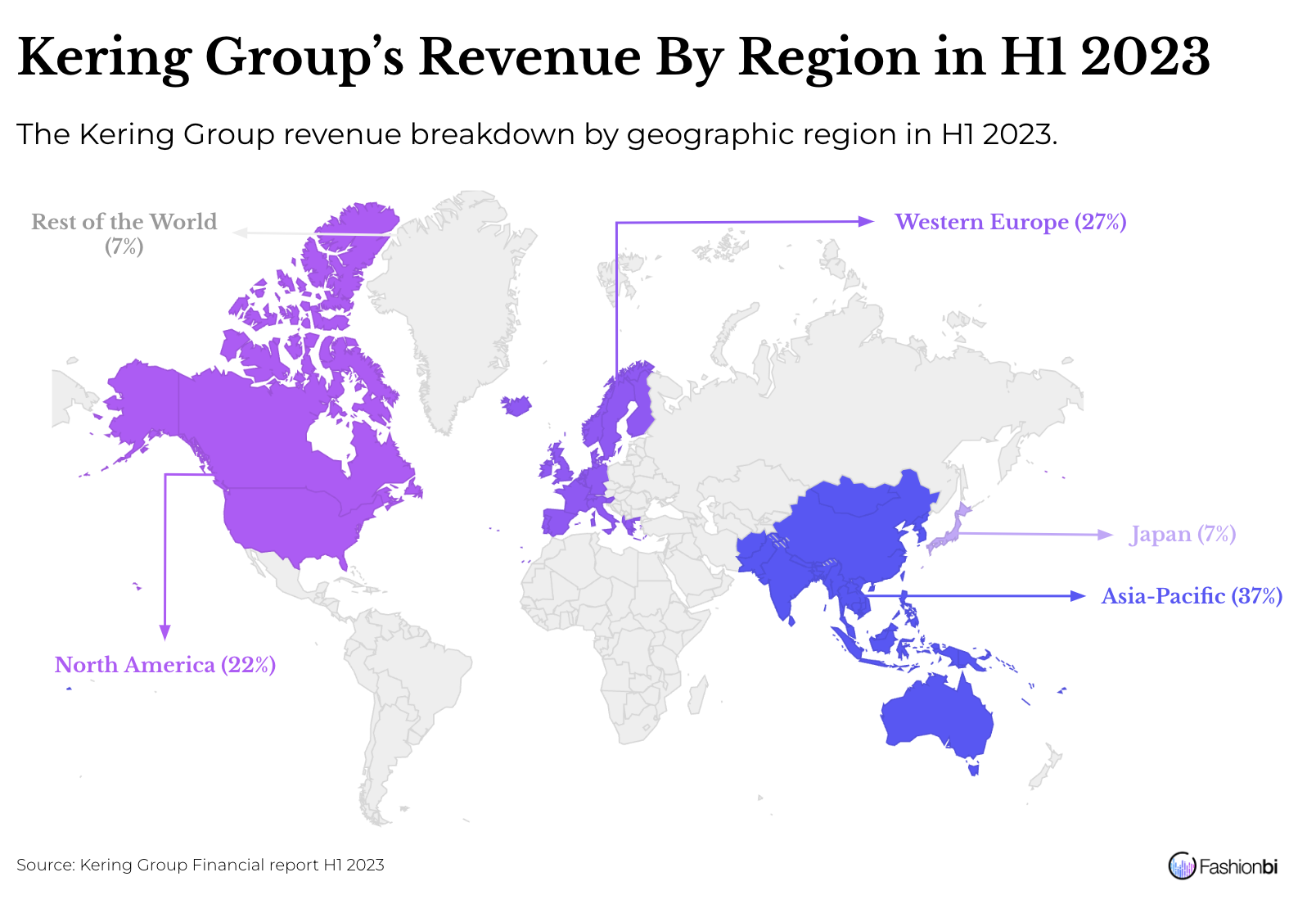

Revenue by Geographic region

In 2022, the group’s revenue faced strong growth in Western Europe with a rise of 36% on a comparable basis. This inclination was mainly due to the local demand and the increase in tourist numbers since the Spring (while the Chinese tourists had a low number). Japan gave a revenue hike of 25% when compared to 2021. In addition to the rise in domestic demand, the Japanese market had a boost driven by its appearance with Asian tourists (due to the weak yen).

The turnover has elevated by 5% in North America. The performance was hindered by the American customers who chose the Western European market and weaker local demand. The Asia-Pacific region earned higher revenue with 33% of the total. Because of China’s zero-Covid policy, the revenue declined by 8% compared to 2021. Growth rates in Southeast Asia are high, especially in South Korea.

In H1 2023, the group’s sales in the Western Europe region increased by 4%. The physical store performance has risen by 18% due to American and Asian tourist numbers. The engagement in local customers is still less and has declined online revenue too. The revenue in Japan has remained stable with a 28% rise between Q1 and Q2. Even though the market benefited due to the weak yen, the sales among local customers are coming back to normal.

Revenue fell by 23% in North America, directly driven by the decline in local demand and less engagement in American customers shifting to Western Europe. Asia-Pacific Region gave a revenue up by 16% with a 26% acceleration in Q2, reflecting the lower foundation for comparison in China. Every market in the region faced a hike in sales except Australia and South Korea. There is still less domestic demand in South Korea as customers are buying products from other regions due to price differences.

Revenue by Distribution Channels

By the end of 2022, the group opened 100 new DOS stores worldwide. The stores were unveiled in regions such as Western Europe (343), North America (278), Japan (239), Asia-Pacific (662) and the rest of the world (137). As a result, the revenue from e-commerce and directly operated stores was at €16.007 million, showing a 10% climb when compared to 2021. This amounted to over 78% of the total sales.

The e-commerce channel is growing at a slow pace with a 11% rise. This increase is driven by the continuing strategy followed by all the brands that focused on managing their distributions effectively and exclusively.

Wholesale distribution sales hold 22% of the total revenue. It has increased by 4% but decreased by 1% on a comparable basis when considering all the brands. This result is due to the group’s undergoing changes in the channel reorganisation by which the group can focus on supporting high-quality distributors. Kering Eyewear showed the most rigid wholesale revenue growth rate of 27% with its improvement in current licences and incorporation of Maui Jim and Lindberg. The royalty and other revenues have soared by 30%.

In the first half of 2023, the group further unveiled 35 new DOS stores around the world. The revenue of DOS and e-commerce channels was €7.868 million with a 4% increase compared to H1 2022. This channel owned 77% of the total sales, driven by the same long-term strategic initiative taken by all the brands in 2022. The e-commerce channel faced a decline due to oversaturation in specific product categories and customer segments which is affected by inflation. Wholesale revenue was 23% with a 8% decline. It fell even more to 16% while considering only the houses. Despite the completion of the streamlining process in Gucci, the group is still in process in other houses. Kering recorded a wholesale sales growth rate of 16% on a comparable basis. The royalty revenue from the licences and other miscellaneous revenue has improved by 14%.

Cover Image: Kering Group's presentation at the 2022 China International Import Expo (CIIE), courtesy Kering Facebook Page